Getty Images/David Crotty It appears that Green Bay Packers quarterback Aaron Rodgers and retired race car driver Danica Patrick were victorious in their bid for a celebrity-pedigreed beachside spread in Malibu, CA, according to Variety. The power couple paid $28 million in cold, hard cash for a 3,592-square-foot home with the famed Pacific Coast Highway on one side and the Pacific Ocean on the other. Real estate records show the home was sold in November. They purchased the property from British pop star Robbie Williams and his wife, Ayda Field, after renting it from the couple over the summer. Originally built in 1981, the compound has gone through several multimillion-dollar renovations. Williams snapped up the property in 2018 for $20.25 million, netting a nearly $7 million profit in a little more than a year. Rodgers and Patrick must have really loved that summer rental.

realtor.com

realtor.com Of course, there’s quite a bit to love. It has only three bedrooms and three baths, but every square inch is stylish and pristine. It’s set on a bluff overlooking the ocean, so high tides are not an issue, and the beach below can be accessed by either a staircase or the property’s own, quaint funicular. There’s no need to schlep their own towels, lounge chairs, snacks, and drinks down to the sand.

realtor.com The sporty couple can enjoy a victory lap in a sparkling pool with a spa, while grilling burgers and dogs on the built-in barbecue. The compound also features extensive decks overlooking the sand and surf.

realtor.com Massive glass doors open to the decks, enabling indoor-outdoor living space. One of the decks features built-in seating, creating a conversation area with spectacular views.

realtor.com

realtor.com Interiors are mostly white, with some cement and wood flooring providing low maintenance and high style. Floor-to-ceiling disappearing doors throughout the house give many rooms, including bedrooms and baths, access to more balconies and decks. Generous, modern casement windows allow in even more light.

realtor.com

realtor.com The main house features an open floor plan with a lounge and game room on the basement level.

realtor.com

realtor.com The property includes a neatly appointed two-bedroom guesthouse and three-car garage, which may or may not accommodate all of Patrick’s speedy vehicles.

realtor.com While $28 million may seem like a massive amount even for such a posh property, rest assured that this athletic A-list couple can well afford it. Rodgers, a 36-year-old California native, has a Super Bowl ring to his credit, and is considered one of the greatest quarterbacks of all time. Proof of that came in 2018, when he signed a record-setting, four-year, $134 million contract extension with the Packers. Meanwhile Patrick, 37, the most successful woman in the history of American open-wheel racing, officially retired in 2018. She has had advertising partnerships with companies such as Secret, Nationwide Insurance, Tissot, Chevrolet, Coca-Cola, Hot Wheels, GoDaddy.com, and Lyft, and has appeared in numerous films and TV shows. And last August, she launched a weekly podcast called “Pretty Intense.” The post Packers QB Aaron Rodgers and Race Car Phenom Danica Patrick Zoom Into a Malibu Mansion appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/aaron-rodgers-and-danica-patrick-zoom-into-a-malibu-mansion/

0 Comments

Justin Sullivan/Getty Images Home prices increased at a slightly faster rate in October, the latest sign the housing market is firming after weakness earlier in the year. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which measures average home prices in major metropolitan areas across the U.S., rose 3.3% in October on an annual basis. That was a marginally greater increase than the 3.2% year-over-year rise during September. The acceleration in home-price growth during October coincides with other data pointing to a pickup in home sales during the second half of the year, amid mortgage rates that are low by historical standards and steady economic growth. “October’s U.S. housing data continue to be reassuring,” said Craig J. Lazzara, a managing director at S&P Dow Jones Indices. “With October’s 3.3% increase in the national composite index, home prices are currently more than 15% above the pre-financial crisis peak reached July 2006.” Prices were up 2.2%, year over year, in large metro areas in a 20-city composite index tracked by S&P, a smaller increase than the rise nationally. The Phoenix area saw the biggest price increases among the 20 large metro areas, with prices up 5.8% year over year. The Southeast region also saw strong gains, according to the report. A separate report from the Federal Housing Finance Agency released Tuesday also showed home prices were up 0.2% nationally in October from the previous month and up 5.0% from the previous October. The National Association of Realtors said earlier this month that existing-home sales were up 2.7% in November from a year earlier, the fifth straight month of year-over-year gains. The post Home Prices Rose at a Slightly Faster Pace in October appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/real-estate-news/home-prices-rose-at-a-slightly-faster-pace-in-october/

Getty Images/Stefanie Keenan It’s no small feat to skip merrily through the sale of a luxury condo in Manhattan these days. But Tamara Mellon, co-founder of the swank Jimmy Choo shoe line, was able to move her Greenwich Village condo for $18.8 million after only about 60 days on the market, according to the RealDeal. Of course, she had to be willing to let the price drop in order for a buyer and the condo to make the perfect pair. She originally tagged the 3,965-square-foot apartment with a starting sales price of $19.8 million, and ended up accepting $18.8 million from an anonymous buyer. The fashion entrepreneur had purchased the three-bedroom, 3.5-bath spread in 2016 for around $18.4 million, so she didn’t exactly make a killing. But she did come out a few steps ahead.

realtor.com But limited time on the market also has value, so the quick sale of the designer pad can be considered a success. The eighth-floor unit with 1,264 square feet of private outdoor space (balconies and decks) is quite in demand in Manhattan, and apparently was of great value to the buyer.

realtor.com And the posh development must have also been a draw. The unit is part of Greenwich Lane, a collection of five unique addresses and five townhouses that take up almost an entire block in the West Village. Homeowners in the complex enjoy ritzy amenities such as yoga and spa treatment rooms, a 25-meter indoor pool with a hot tub, a high-end golf simulator, and a spacious residents’ lounge.

realtor.com There’s also a dining room with a chef’s kitchen and separate catering kitchen, a 21-seat screening room, playroom, courtyard with fountain, extra storage, and lobbies with 24/7 staffing.

realtor.com The development was completed in 2013, but Mellon has obviously spent a bit of time updating it since then, if nowhere else than in her massive closet, which accommodates an extensive footwear collection. Really, can you ever have too many pairs of black boots? Not in this shoe heaven.

realtor.com Other luxe features include wood floors, a huge great room with high ceiling, and floor-to-ceiling windows and glass doors, which feature views of Greenwich Village on two sides.

realtor.com In fact, most of the rooms in the unit, including some baths, have walls of windows and doors that look out onto remarkable views of the city.

realtor.com

realtor.com Along with a dining area in the great room, the home has an eat-in kitchen, featuring an island with seating and a breakfast area (also with views). And the professional-grade, stainless-steel appliances would make any chef’s mouth water.

realtor.com Mellon co-founded the iconic shoe company with designer Jimmy Choo himself in 1996, but parted ways with him in 2011. She then started her own eponymous Tamara Mellon shoe line. The Real Deal reports that Mellon also owns a Manhattan penthouse duplex measuring 7,140 square feet, which is currently on the market for $25 million. The post Co-Founder of Jimmy Choo Struts Through a Quick $18.8M Sale of Her Luxe NYC Condo appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/co-founder-of-jimmy-choo-struts-through-a-quick-18-8m-sale-of-her-luxe-nyc-condo/

tupungato/iStock The numbers: The index of pending home sales increased 1.2% in November from the previous month, the National Association of Realtors reported Monday. In October, sales had fallen after two consecutive months of increases. The index records transactions that have not yet closed but where a contract has been signed. As a result, the index serves as an indicator for existing-home sales reports in the coming months. What happened: Compared with November 2018, contract signings were up 7.4%. The index is benchmarked to contract-signing activity in 2001. Sales in the West increased substantially by 5.5%, while contract signings only saw marginal changes in the Northeast (down 0.1%), South (down 0.2%) and Midwest (up 1%). When compared with last year, sales were up in all four regions. Big picture: The positive November data aside, the inventory of homes for sale will remain a challenge. “Despite the insufficient level of inventory, pending home contracts still increased in November,” said Lawrence Yun, chief economist for the National Association of Realtors. “The favorable conditions are expected throughout 2020 as well, but supply is not yet meeting the healthy demand.” In October, Yun said that the lack of inventory contributed to the downturn in pending sales, arguing that buyers were having a difficult time finding homes available for sale. While most economists expect home-building activity to gain steam next year, it won’t be enough to fully meet the demand that’s in the market. As a result, home prices should continue to increase at healthy — if somewhat slower — pace. Mortgage rates are anticipated to remain at their current, historically-low levels in 2020, but that may not be enough to make buying a home affordable for would-be buyers struggling to get enough money together to make a purchase. Market reaction: The Dow Jones Industrial Average and the S&P 500 fell from record levels Monday morning, while the 10-year Treasury note’s increased. The post Pending Home Sales Rebound 1.2% in November Led by Resurgence in One Region appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/real-estate-news/pending-home-sales-rebound-1-2-in-november-led-by-resurgence-in-one-region/

realtor.com Sure, we get that the nearly $20 million price tag on this property sounds like a lot. But once you eye this contemporary oceanfront Maui mansion in Kihei, HI, currently listed for $19,995,000, we think you’ll agree that this piece of paradise is worth every penny. The one-of-a-kind home, designed by architect Guy Dreier, was completed in 2006. The organic and sculptural five-bedroom, 5.5-bathroom, 9,176-square-foot space is described in the listing as a “livable work of art.” It certainly has the perfect tropical setting, which the design leverages. On the main level, the open floor plan features several living and dining areas overlooking the pool and jaw-dropping views of the ocean. And the owner’s suite as well as all three guest suites open to their own private ocean lanais. The roomy half-acre lot includes decks, a pool, and lush landscaping.

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com Once a favorite destination of Hawaiian royalty, Kihei is on the southwest shore of Maui, where conditions are sunny and dry—the perfect spot to build a dream home for a well-heeled client. The estate is situated in a cove on the Makena Maui shoreline, and the home’s design gives the sense that it’s floating above the waves and rocks churning below. Dreier’s modern, sweeping design in Palm Desert, CA, won the Robb Report 2009 Home of the Year honors. Dreier has built many luxury homes across the world, including some spectacular estates in Rancho Santa Fe, La Jolla, and Malibu in California, and Saudi Arabia. The post $20M Maui Mansion Is a Must-See Modern Hawaiian Fantasy appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/unique-homes/20m-maui-mansion-is-a-must-see-modern-hawaiian-fantasy/

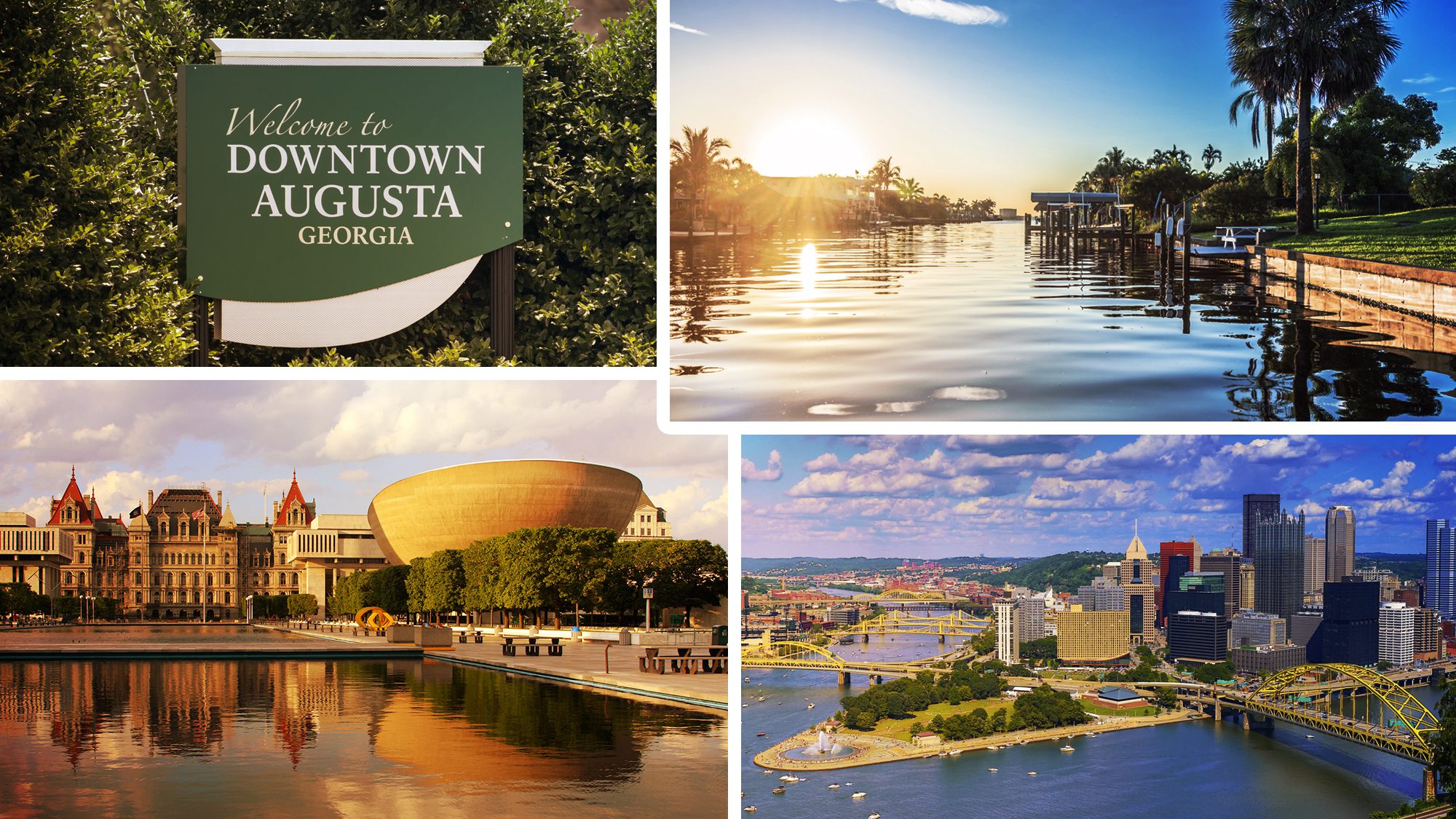

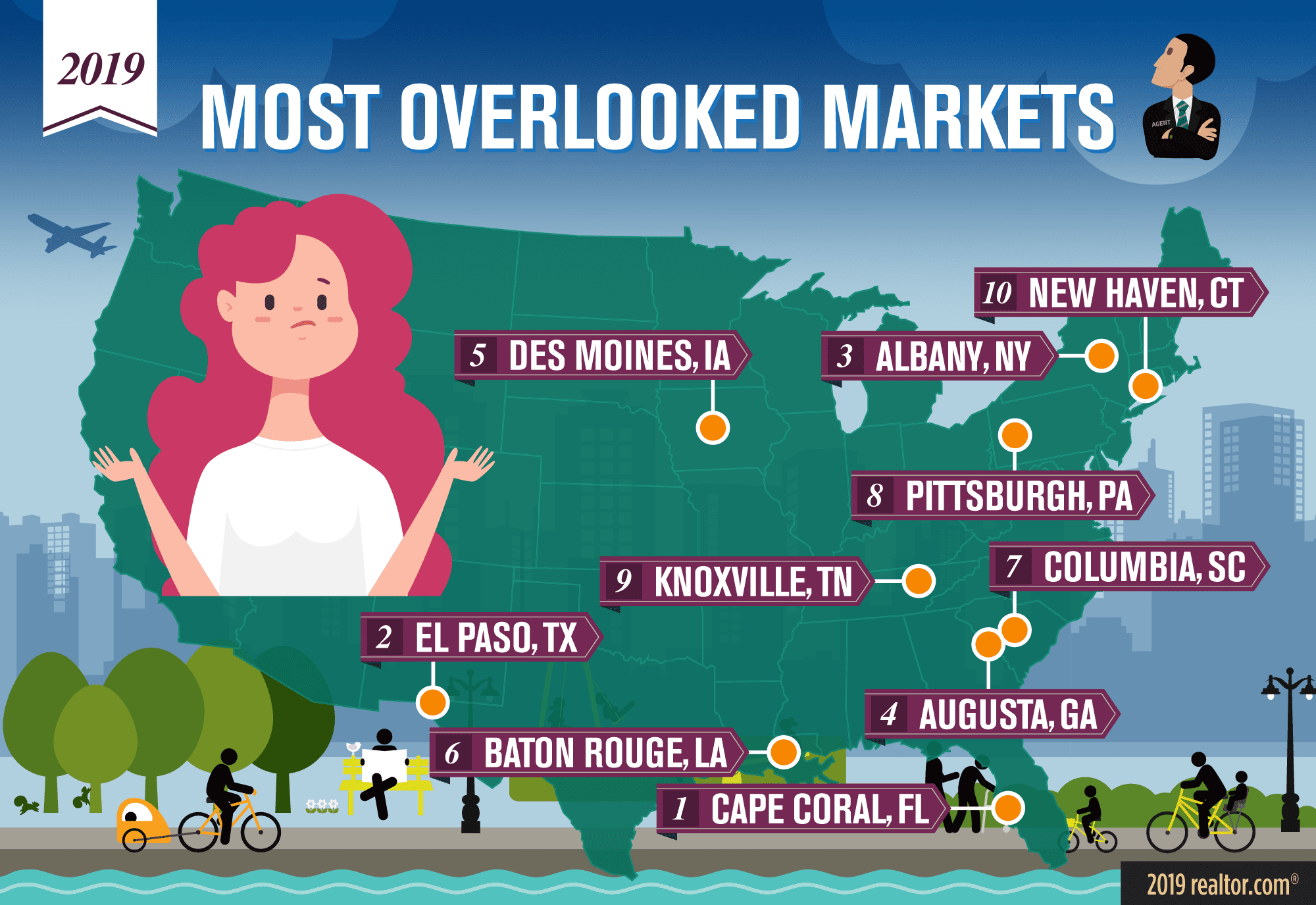

Augusta, GA; Cape Coral, FL; Pittsburgh, PA; Albany, NY Everyone loves to discover a real bargain, whether it’s a discounted lunch special, a mysteriously cheap laptop, or a home. Especially a home! The sad truth: While we all tend to obsess over the nation’s famously desirable, famously overpriced markets—San Fransisco and New York and Denver, oh my—they don’t exactly offer a lot of unexpectedly affordable housing options. And along with the stratosphere-scraping prices comes crazed competition among buyers. Who needs the drama? Don’t despair! None of this means you have to put your homeownership dreams on hold. In fact, there are places where you can land your ideal home for a low price, where homes don’t go off the market in a matter of minutes, and where you can still find plenty of fun things to do. But they just might not be the first places you’d think of. That’s why our trusty data team members put on their headlamps and most durable duds and started digging, working to uncover the most overlooked housing markets—the hidden places where buyers can score a deal on a home and land a good job, all without dying of boredom. After all, seeking out a mellower market can save your sanity and open up options. “In a really hot housing market you might have to buy a home quickly, make an offer that’s more competitive with a larger down payment, or waive contingencies you might prefer to keep,” says Danielle Hale, chief economist of realtor.com. “It’s less likely you might have to make those concessions as a buyer in a colder market.” To figure out where buyers can get into the housing market without raising their cortisol levels (too much), realtor.com’s team of treasure hunters looked at the metro areas with the following:

We limited the list to just one metro per state and ranked them in order of longest days on the market. “Even though properties are sitting on the market in many of these areas, values are still increasing,” Hale says. So let’s take a stress-free ride across the country, and check ’em out.

Tony Frenzel 1. Cape Coral, FLMedian home list price: $299,950

realtor.com Set on the Gulf of Mexico in serene Southwest Florida, Cape Coral boasts 400 miles of canals where homeowners can tie up a boat behind their own home and fish from their own dock. Those beautiful inland waterways were overtaken with toxic foul-smelling, blue-green algae blooms after Hurricane Irma swept the area in 2017, which took its toll on home prices for a couple of years. But the Army Corps of Engineers has been testing water filtration systems to collect and remove those sorts of deadly algae blooms in the future—and, as a result, buyers have been slowly creeping back into town to pick up deals. “We haven’t had any problems this year, and my phone has been ringing off the hook,” says Mike Lombardo, broker with Old Glory Realty. For less than $300,000, it’s possible to score a home with Gulf access, like this three-bedroom, two-bathroom place—as well as newly remodeled places with pools, higher square footage, and waterfront views for right around the same price. 2. El Paso, TXMedian home list price: $187,725

realtor.com El Paso made headlines when it was shaken by a mass shooting in August, and the emotional impact is still being felt. But by all economic measures, things have been looking up in recent years for the Texas border town that sits right at the crux of Las Cruces, Ciudad Juarez, and Chihuahua City. The population is growing fast, recently hitting 800,000. The Mexican peso has gained strength on the U.S. dollar, helping the borderland economy hit $13 billion in commercial activity. And home values are creeping up—11% over last year, according to recent realtor.com data. “When I moved here five years ago, it was a very different city from what is now,” says Alex Cordova, real estate agent with Alexander Cordova Luxury Real Estate. “It’s a huge, booming city right now.” The military town has also been transforming into a bigger college town with a broadened research program at the University of Texas at El Paso. To serve all the young residents, the city boasts more than 1,000 restaurants and bars along with 35 museums. In the desirable neighborhood of Castner Heights, buyers can get three-bedroom homes, in a variety of styles—from Colonial and Pueblo Revival to ranch—for $175,000 (or less). Or you can land a brand-new, four-bedroom home for just $229,900. 3. Albany, NYMedian home list price: $294,950

realtor.com Outdoor enthusiasts, rejoice! Along with its whopping 1,331 restaurants and bars, 46 museums, and a thriving indie music and arts scene, come wintertime Albany offers more sledding, ice skating, snowmobiling, and tubing per capita than just about any other metro in the U.S. Still, Albany still has plenty of deals on homes—you can get into a three-bedroom restored historic home in the desirable Pine Hills neighborhood for $189,000. “You can get a really nice house in the city within walking distance to restaurants and bars,” says Anthony Gucciardo, broker at Gucciardo Real Estate Group. While the state capital and college town has started marketing itself as a tech hub—gaining some good-paying biotech, engineering, and pharmaceutical gigs—the city has had its share of economic struggles over the past few decades. It has kept homeownership rates low: According to the U.S. Census Bureau, only 37.2% of all housing units are owner-occupied. But a never-ending supply of college students searching for housing also makes Albany a prime opportunity for potential buyers who want an investment property and need a strong pool of renters. A lot of empty nesters and first-time buyers pick up deals in coveted neighborhoods like the aforementioned Pine Hills and Buckingham Pond, a vibrant, walkable area with tons of eateries. 4. Augusta, GAMedian home list price: $224,285.5

realtor.com Augusta might be most famous for the Masters golf tournament—and its legendary pimento cheese sandwich—but it has way more to offer than an annual sporting event. The historic city founded in 1736, on the beautiful banks of the Savannah River, is just two hours from Atlanta and two hours from the coast. Over the past couple of years, the military town has diversified its economy with medical and manufacturing jobs, like E-Z-Go golf carts, and opened a U.S. Army Cyber School in Fort Gordon. The town’s unemployment rate has dropped substantially, from 5.8% (a couple of points higher than the national average) in 2016 to 3.3%. But that’s not all—Augusta boasts more than 700 restaurants, 14 museums, and a wide range of homes that cost a fraction of the price of other Georgia metros. Buyers can score a charming four-bedroom Colonial, just 10 minutes from the city’s famed 18 holes, for just shy of $250,000. 5. Des Moines, IAMedian home list price: $292,550

realtor.com Des Moines, quite simply, is thriving. The city’s population has increased 6.2% since 2010, drawing a plethora of young professionals who come for jobs in the large financial, insurance, and publishing sectors, with offices for Wells Fargo, Nationwide, and Meredith Publishing. And those white-collar workers are staying for the amenities. Des Moines boasts 1,000-plus restaurants, an annual arts festival, and regular concerts on the river that feature bands such as Edward Sharpe and the Magnetic Zeros and Foster the People. “In the last 10 years, the city’s culture has shifted to very artsy,” says Tim Scheib, a Realtor® with Re/Max Precision. Because of the thriving economy (the unemployment rate is just 2.5%), developers have been working on a wide array of housing projects for every level of the market. For instance, to the west of the city, a project called Kettlestone is currently underway. The 1,500-acre, mixed-use development features a range of residential housing, restaurants, and offices connected by trails, parks, and ponds. In this community you can score a three-bedroom home for under $300,000. “These kinds of areas are attracting a lot of families and young couples preparing for a family,” Scheib says. Those who want to be in the heart of the city—and care less about space—can find industrial-style, one-bedroom condos starting around $145,000. 6. Baton Rouge, LAMedian home list price: $247,446

realtor.com Even though Baton Rouge has seen an influx of restaurants and bars (it has more than 1,100 listed on Yelp) in its walkable downtown, the high-in-crime state capital has been losing population. But as many city dwellers have decamped for the suburbs, the larger metro’s overall population is up 3.6%. The first-time buyers and young families moving to burbs can get a large four-bedroom, French-inspired home for $275,000, smack dab in the middle of the desirable Ascenscion Parish school district, just minutes away from the city These areas are full of historic buildings and Spanish moss–covered oak trees as well as lots of parks and waterways. And, since it is Louisiana, there’s excellent Cajun- and Creole-style fare. While home values have increased about 4% from last year, the market is still better for buyers than it was a couple of years ago. Catastrophic flooding in 2016 decreased the area’s housing stock, causing home prices to surge as a result. “There was a huge demand for housing with multiple offers taking place per listing,” says David McKey, broker with Coldwell Banker One. “We’re back to a more normal market now.” 7. Columbia, SCMedian home list Price: $239,950

realtor.com South Carolina’s state capital might not get the attention of its darling coastal sister, Charleston, but it still has plenty of respectable amenities—and its housing is far more affordable. Charleston’s median list price of $325,000 is nearly $100,000 higher than Columbia’s. Columbia boasts a solid mix of global companies like BlueCross BlueShield, students and educators at the University of South Carolina, and a large military base. The city has nearly 750 restaurants (including some award-winning barbecue joints) and 32 museums. The crime levels within city limits remain a problem point—the city was ranked as the 25th most dangerous city in the U.S.—but some of the surrounding towns are statistically much safer, and still affordable. For instance, in the nearby suburb of Lexington, buyers can get a new three-bedroom, 2.5-bath Colonial Revival home for right around $230,000. The town attracts young professionals and families with its highly rated public schools, multiple parks and nature preserves, and its own fun winery. 8. Pittsburgh, PAMedian home list price: $189,750

realtor.com After years of industrial decline, Steel City has become the poster child for urban renewal. It’s now a tech hot spot and medical hub, and it regularly comes up on national lists of best cultural and dining destinations. The city of 300,000 residents has a staggering 1,800-plus restaurants—offering everything from vegan pierogies to award-winning Basque cuisine—and 129 museums, far more than any of the other cities on this list. All that revitalization doesn’t make up for the fact that the city is still bleeding population. Since 2010, the city lost 1.4% of its population, according to the U.S. Census Bureau. But here’s the thing: Fewer people means more housing options for buyers—and better deals. Techies and other young professionals have been snatching up large homes in Brighton Heights for a steal, like this historic five-bedroom for $199,000. “The basic story is the death rate is higher than the birth rate,” says Bob Strauss, professor of economics and public policy at Carnegie Mellon University, who says the net in-migration hasn’t caught up to the existing housing stock. “But what you’ve got in Pittsburgh is a relatively safe, culturally diverse, and affordable place to live.” Buyers who want to enjoy all of Pittsburgh’s cultural capital can get some serious deals in hip enclaves like East Liberty and Lawrenceville, where you can get a redone three-bedroom row house for just $239,900. 9. Knoxville, TNMedian home list price: $284,425

realtor.com With its burgeoning downtown scene and location nestled near the Great Smoky Mountains, Knoxville has been drawing new residents in recent years. Its population has increased 5.2% over the past decade thanks to its temperate climate, lower cost of living, and an unemployment rate of just 2.6%. That growth has led to a steady run-up in home prices in the college town, with sellers getting about 99% of their asking price through much of 2018, according to local real estate agents. That might seem like a deterrent—and indeed, entry-level homes are still flying off the market. But houses in the $300,000-plus range are sitting around longer—for somewhere between 90 to 120 days, says Glenda Johnson, broker-agent at Coldwell Banker Jim Henry. That means buyers who have a higher budget are poised to score a sweet home for a steal, like this three-bedroom Colonial in the popular Seven Springs subdivision. 10. New Haven, CTMedian home list price: $279,050

realtor.com After decades of decline in manufacturing jobs and languishing downtown retail, New Haven’s population has been on a slow uptick for the past several years, and unemployment is finally below the national average at 3.1%. The median days on market in the home of Yale—which along with a nationally regarded theater scene happens to have the best clam pizza on the face of the earth (yes, really)—is on par with the national averages. Like many other college towns, much of New Haven’s population is driven by transient students and faculty: Only 27.8% of housing units are owner-occupied. That means buyers can pick and choose from a wide array of historic homes priced around $300,000 in fun areas like Wooster Square, like this chic three-bedroom loft in a sun-drenched warehouse for $335,500. The market has been seeing a lot of action recently with tons of investors who have taken note of the growing strength of the market, says Jack Hill of Seabury Hill Realtors. “It’s a great little city.” The post Hidden Gems: The 10 Most Under-the-Radar Markets Where Buyers Can Score a Fantastic Deal appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/most-overlooked-markets-where-buyers-can-score-a-fantastic-deal/

Joe Scarnici/Getty Images for Theatre Box; realtor.com Scott Disick, Kourtney Kardasian‘s ex and star of the successful new home renovation show “Flip It Like Disick,” appears to be at it again. He recently purchased a rather dated home in “Kardashian Country,” aka Hidden Hills, CA, for $3,106,000. And it looks highly flippable. Built in 1977, the 4,602-square-foot home sits on an acre lot. It has four bedrooms and 4.5 baths. But that could all change once he and his partner in design, former pop singer-turned-interior designer Willa Ford, get their hands on it. The house has great bones and vaulted ceilings, but there’s still a lot to be done to bring it into the 2020s. We’re guessing the first things to go would be a wall or two in what could become a wide-open great room. The next would be the terra-cotta floor tiles and all those pesky split levels.

realtor.com

Scott Disick's latest purchase in Hidden Hills We also think a lot can be done with the kitchen, which will doubtless be expanded and get lighter, more modern cabinets and hardware. But the appliances could stay, as they’re newer high-end Wolf and GE Monogram, including a six-burner stove, warming drawer, double ovens, and double-drawer dishwasher.

realtor.com In addition, there’s a lot to work with in the large master suite, with its fireplace, built-in window seats and bookcases, and double walk-in closets. The en suite bath offers a large jetted tub, separate steam shower, and dual vanities. With space like that and a decent budget, the possibilities are endless. But we would start with removing the odd arched alcove.

realtor.com

realtor.com Then there are choices to be made about what stays and what goes outdoors as well. We’re guessing the chicken coop is not going to be a keeper. But the built-in, shaded fire pit conversation area will probably survive the renovation, as well as an adorable treehouse.

realtor.com

realtor.com We’re also betting that the dozens o fruit trees will stay, and that something very creative will be done with the detached studio/office/theater room. It’s notable that Disick’s latest purchase is just down the street from his most recent remodel. He bought that 5,663-square-foot luxury home for $3,235,000 in April 2018. And after completely remodeling it in his typical stylish fashion, he put it on the market in September for $6,890,000. Are you sensing a pattern here? Stay tuned! The post Scott Disick to ‘Flip It’ in Hidden Hills Again? appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/scott-disick-to-flip-it-in-hidden-hills-again/

Le Belvedere | David O. Marlow At the dawn of this decade, the U.S. was reeling from a real-estate crash and the worst economic downturn since the Depression. Home prices in some regions were starting to recover, but it seemed impossible that values would return anytime soon to their dizzying boomtime highs. Few could have predicted that within a few years, the luxury market would not only recover but reach a staggering new height. A tidal wave of global wealth poured into U.S. real estate after the 2007-09 recession, creating in the 2010s a new segment of the market: ultraluxury homes targeted at the global billionaire elite. Pricier and more lavish than anything that came before them, these homes had outsized amenities such as commercial-grade hair salons, hotel-worthy spas and home theaters with concession stands. As the extreme became commonplace, homeowners began to add more attention-grabbing features, such as shark tanks and private nightclubs. Meanwhile, luxury-condominium buildings grew taller than ever. Standing 1,550-feet high with 131 stories, Central Park Tower in Manhattan is now the tallest residential building in the world. Today, because so many buyers are wealthy enough to withstand the most severe economic swings, this new sector largely acts independently from the broader real-estate market. So while the number of sales are falling in many luxury markets across the country, six homes in the U.S. have closed for $100 million or more so far in 2019—the highest number for a single year. In 2010, there were none. That year, the highest sale price was $50 million (plus about $2 million of furnishings) for Le Belvedere, a Bel-Air mansion with a swan pond and a ballroom that could seat more than 200 people.

David O. Marlow “People don’t realize that there are two markets happening in the world,” said Oren Alexander, an agent at Douglas Elliman Real Estate. “We’ve been hearing that things have slowed down, and that’s true—no doubt about it. But the unique, one-of-a-kind, top-notch product? That market is doing better than ever.” Home sales of $50 million or more used to be an anomaly, with two or less each year in the early 2000s, according to Miller Samuel, a residential appraisal and consulting company. In 2014 that figured spiked to 23, and hasn’t fallen below 12 since. In Los Angeles, the average home-sales price soared 153% to $2.5 million between the third quarter of 2009 and the same quarter of 2019, according to Miller Samuel. Florida’s ritzy barrier island of Palm Beach saw its average home price surge 77% in that same period, while Miami’s jumped 72%. Manhattan, which has stumbled in recent years, still had an average sales price of $1.65 million in the third quarter, 25% higher than the same quarter 10 years earlier. A decade that will be remembered for its excesses, the 2010s saw the first-ever condo sales topping $100 million, then $200 million. In the 2010s billionaires bought not just one, but multiple $100 million-plus homes for themselves. Some buyers paid tens of millions of dollars for houses, only to raze them and build brand-new mansions in their place. They bought newly constructed, multimillion-dollar condos and gut-renovated them, putting existing high-end finishes out with the trash. They upholstered their walls in red leather from the uber-luxury handbag brand Hermès. The youngest members of the family got playhouses that cost more than conventional homes. The postrecession flood of buyers has now slowed, and far more home sellers seek nine-figure price tags than actually achieve them. Still, it is clear that ultraluxury sales are now a fixture of the marketplace. The $100 million sale “is now a thing,” said real estate appraiser Jonathan Miller of Miller Samuel. “This will not go away.” In the 2010s, hedge-fund billionaire Ken Griffin poured at least $820 million into home purchases in New York, Palm Beach, Chicago and London. Since 2011, Facebook CEO Mark Zuckerberg has spent at least $250 million on real estate. Embattled WeWork founder Adam Neumann has paid about $90 million for six homes since 2012, including a California estate with a guitar-shape living room. Natural gas billionaire Michael S. Smith paid $110 million in 2018 for an oceanfront compound on Malibu’s Carbon Beach. What Mr. Smith paid is more than 1,500 times the U.S. median household income for that year, or $63,179, according to census data. It’s enough to buy 550 Ferraris, or more than 450 houses priced at $243,225, the current median value of a home in the U.S. “These are numbers that mere mortals don’t pay for housing,” said Mr. Miller. How did we get here?

Lisa Corson for The Wall Street Journal Back in 2010, Uber and Airbnb were fledgling startups. Instagram had just launched. Many people used Amazon.com primarily for buying books. Many tech companies have seen expansive growth since then, yielding massive amounts of wealth for their founders. Meanwhile, vast fortunes were created in emerging economies across the world, such as China, Russia and Brazil. “Over the last 10 years, we’ve seen a recovery from the financial crisis and a long boom in stock prices,” said Maya Imberg, director of Thought Leadership and Analytics at Wealth-X. “That’s pushed up the overall amount of wealth in the world.” In 2009 there were 174,000 people world-wide with a net worth of $30 million or more, according to Wealth-X. By 2019 that number had jumped to 275,000. This generation of affluent people has eagerly purchased luxury real estate in their home countries and around the world to diversify their assets or escape political instability at home, said Liam Bailey, head of Knight Frank’s residential-research team. “Wealth has become much more mobile,” he said. “The new wealth that has been created in emerging markets in particular has a very global outlook.” Today, he added, international ultrahigh-net-worth individuals typically have at least three or four homes in multiple cities outside their home country. With interest rates low after the financial crisis, “investors were running around the globe investing in real estate as a way to generate higher returns,” Mr. Miller said. “It was a frenzy.”

realtor.com A key turning point came in 2012, when former Citigroup Chairman Sandy Weill sold his penthouse at Manhattan’s 15 Central Park West for $88 million—roughly twice what he had paid for it in 2007—to Russian billionaire Dmitry Rybolovlev. That deal “opened up a whole new echelon of what could be,” said Corcoran chief executive Pamela Liebman. With land prices high and credit tight in the wake of the recession, developers buoyed by investment dollars built almost exclusively high-end product, Mr. Miller said. The result was an “explosion of luxury new builds” in cities such as New York, London and Los Angeles, said Mr. Bailey, reversing an earlier trend where buyers would pay a premium for established, old-money buildings. “It almost created a brand-new marketplace.” In Manhattan, for example, new-construction luxury towers like One57 sprang up on what is now called Billionaires’ Row, taking advantage of new technology to build taller buildings than ever before as they competed to lure wealthy international buyers. “You’ve got this arms race between developers, who are using architecture and design to stand out from the crowd,” Mr. Bailey said. “You end up with these incredible buildings.” In 2014, tech entrepreneur Michael Dell set a new Manhattan record when he bought a condo at One57 for $100.47 million. In 2015, an investor group led by billionaire hedge-fund manager William Ackman paid $91.5 million for another unit in the same building. In 2017, an unknown buyer paid $91.1 million for a penthouse at 432 Park Avenue, a nearly 1,400-foot-high tower on Billionaires’ Row. The past decade will be known for redefining luxury, as developers sought to wow buyers by piling on the most over-the-top features. “The amenities have doubled and quadrupled,” said Manhattan real-estate agent Richard Steinberg. It was the decade when sellers put homes on the market with Lamborghinis, Warhols and Picassos included in the asking price. It was the decade when Miami’s Porsche Design Tower was built with glass-walled garages adjacent to the units and accessed by a specially designed car elevator, allowing residents to park just outside their apartments, even 60 stories in the air. In 2017, a Beverly Hills spec house was listed for $100 million with a Champagne vault filled with 170 bottles of Cristal, and a full-time house manager whose salary had been prepaid for two years.

Dorothy Hong for The Wall Street Journal That same year, a Los Angeles spec house dubbed Billionaire hit the market with two fully stocked wine cellars, a candy room filled with treats from Dylan’s Candy Bar and an elevator clad in crocodile skin. The lower level had a four-lane bowling alley with bowling shoes in various sizes. The house sold this year for $94 million. In Boston, the under-construction St. Regis Residences will offer buyers personal butler service and the option of having a watch-winder in the closet. “Always reliable and faithful, your butler will come to understand your exact preferences and even anticipate your needs,” the website boasts. Features now routine in high-end properties, like home automation systems, weren’t long ago considered “super luxury and unattainable to the average person,” said real-estate agent Catherine Marcus Bassick. “What defined luxury in 2009 is not the luxury we would describe now.”

Kim Raff for The Wall Street Journal The post The Decade of the Uber-Decadent House appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/the-decade-of-the-uber-decadent-house/

David M. Benett/Dave Benett/WireImage You may know Steven Zaillian as the Academy Award–winning screenwriter who penned the scripts for acclaimed films such as “Schindler’s List,” “Gangs of New York,” and, most recently, “The Irishman.” But he’s hoping to write a new chapter for his real estate—with a $14,000 monthly lease on his Spanish Colonial Revival–style home in Santa Monica, CA. Charmingly rustic on the outside, with all the modern conveniences inside, the four-bedroom, three-bath home was originally built in 1924 by John M. Chapman, and was owned by abstract expressionist painter Richard Diebenkorn. It has, of course, been updated to its current pristine condition, with due consideration given to its historic and artistic charm.

realtor.com The house measures 2,266 square feet, and has all sorts of unique characteristics, including the curved corner fireplace in the living room, and the graceful casement windows and door in the dining room.

realtor.com

realtor.com Also delightful are the original French doors throughout the house. The skylights in the open kitchen and elsewhere allow plenty of California sunshine to flow through.

realtor.com

realtor.com The bedrooms are also intriguing—one has an inviting reading loft, and another is a light-filled, tile-floored room that could do triple duty as an office, sunroom, and studio. You can’t help but speculate about the riveting screenplays that may have been crafted there. Inspiration abounds.

realtor.com

realtor.com The generous lot features mature landscaping and space to entertain.

realtor.com The property is within walking distance to the Santa Monica Canyon restaurants, as well as the beach. Zaillian, 66, won an Oscar for his screenplay for “Schindler’s List.” He’s also penned “The Falcon and the Snowman,” “Mission: Impossible,” “Hannibal,” and the recent drama “Deep Water.” He both wrote and directed “Searching for Bobby Fischer,” “A Civil Action,” and “All the King’s Men.” He’s already been nominated for both the Critics’ Choice and Golden Globe Awards for “The Irishman” screenplay, which he wrote. The post Screenwriter Steven Zaillian Looking to Write a New Lease on His Home appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/screenwriter-steven-zaillian-looking-to-write-a-new-lease-on-his-home/ Most Expensive New Listing: A $24M Property in Suburban VA That Hasnt Even Been Built Yet12/27/2019

realtor.com A $24 million property in suburban McLean, VA, which has yet to be built, is this week’s most expensive new listing on realtor.com®. The 1.51-acre lot is located approximately 10 miles from Washington, DC, and it last changed hands in 2011 for $1.3 million. Permits have been approved for a lavish, 15,000-square-foot design, and construction will begin in February or March 2020, according to listing agent Fouad Talout with Long & Foster McLean. “We’re not waiting for the buyer,” he says. “If a buyer comes along now, they could choose some of the finishes. That property is going to be completed the same way that it’s being concepted right now. What you see in the photos will be used.” The photos are renderings of what the final project will look like.

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com When complete, the dwelling by Custom Design Concepts Architecture + Interiors will feature six beds and eight baths. Standout flourishes include a domed reception hall, formal dining room, formal living room, and guesthouse. The layout also features a rec room, home theater, and family room. Outside there will be multiple decks, a covered patio, and pool. There will be garage space for 10 vehicles. Talout notes that the home is being designed with an international buyer in mind, starting with its steel framing and construction in a European style. “The exterior of the house is going to be like a French-style chateau, which is timeless,” he says. “It brings the best of both worlds—the modern interior, plus the timeless design exterior.” Another key selling point is the exclusive locale, which has been home to members of the political elite, including former Vice President Dick Cheney and former Secretary of State Colin Powell. And with construction about to start, all the place needs is a well-funded buyer to turn this house into a home. The post Most Expensive New Listing: A $24M Property in Suburban VA That Hasn’t Even Been Built Yet appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/most-expensive-new-listing-a-24m-unbuilt-property-in-va/ |

About usI am Casey Abby From USA and I am 30 Year Old. I done my study recently in MBA Marketing. Archives

April 2021

Categories |

RSS Feed

RSS Feed