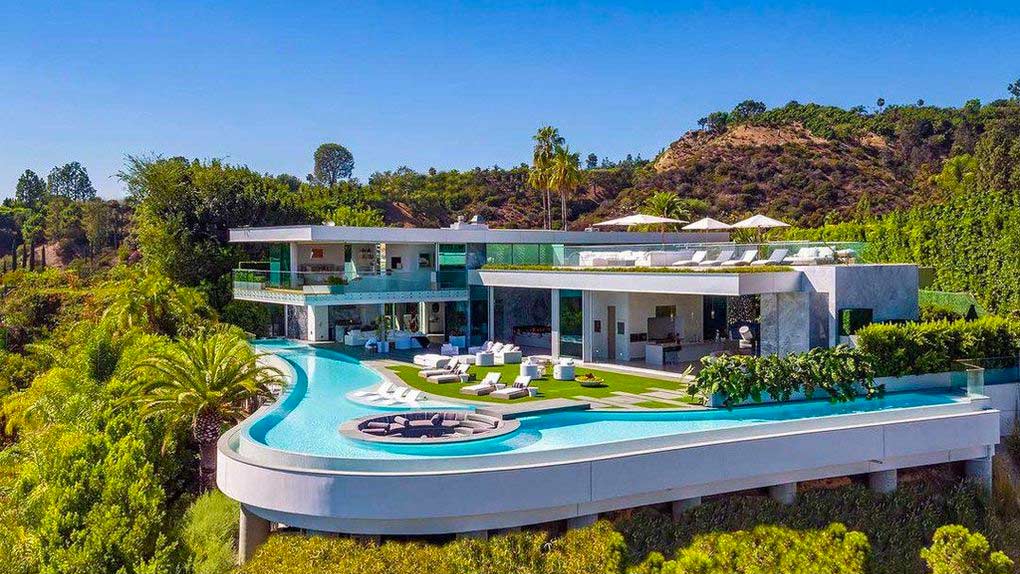

The Weeks Most Expensive Listing Is a $52M Megamansion With the Coolest Pool Weve Ever Seen3/28/2019

realtor.com A luxury home in Los Angeles almost always comes with a pool. And you can bet we’ve seen quite a few high-end versions, from indoor to edgeless. But this week’s most expensivenew listing might just take the grand prize for our favorite pool yet. Behold, the megamansion with a dramatic L-shaped water feature cantilevered over the property. In addition to the dramatic setting and panoramic city views, there’s a cool conversation pit with a fireplace—sunken, literally, right in the middle of the pool. The 16,000-square-foot estate is going for $52 million. Built just last year, the pricey contemporary offers six beds, 10 baths, and all the luxury amenities imaginable.

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com Canadian billionaire and spec developer Francesco Aquilini picked up the property in 2012 for $8,525,500. The grounds had once been the site of a 1960s midcentury modern with its own bragging rights—at one point, the 3,000-square-foot abode had been offered as a rental for $15,000 a month. After Aquilini bought the property, he tapped architect Paul McClean to create his vision for the home. Construction wrapped in 2018, during which time the home was quietly shopped around for $58 million—but had no takers. Now, upon completion, it’s back with a (very moderate) price cut. But those at the top of the market might find this sleek space just the ticket. You can enter the gated hilltop home, billed as a “next generation masterpiece,” by a floating footbridge and glass double doors. Inside, of course, there are plenty of wow-worthy features. In addition to the posh living space, dining room, open kitchen, and family room, disappearing glass walls highlight the home’s seamless indoor-outdoor flow. Plus, there’s a “sumptuous” master suite with a to-die-for bath on the upper level. The lower level is also worth a peek. Downstairs, find a media room, lounge, wet bar, gym, glassed wine room, car display area, and wellness studio. Branden Williams of Hilton & Hyland holds the listing. The post The Week’s Most Expensive Listing Is a $52M Megamansion With the Coolest Pool We’ve Ever Seen appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/most-expensive-new-listing-megamansion-with-cool-pool/

0 Comments

Ty Wright/Bloomberg via Getty Images Mortgage rates are fast approaching 4%, a rate low enough that economists and lenders believe it will help jump-start the housing market again. The average rate on a 30-year fixed mortgage fell to 4.06% this week, its lowest since January 2018, according to data released Thursday by Freddie Mac, the mortgage-finance giant. The rate was down nearly a quarter point from a week earlier, its biggest drop in over a decade. In many cases rates are lower than 4%. Lenders advertising mortgages at sub-4% rates this week include Toronto-Dominion Bank, HSBC Holdings Plc and Teachers Federal Credit Union, according to Bankrate.com. Just a few months ago, average rates were on the verge of hitting 5%, drying up refinancings and putting a damper on home price growth. While the housing market remains cooler than it had been at its peak, lower mortgage rates are again raising hopes for a rebound as the spring selling season gets under way. Mortgage rates have been declining along with the yield on the benchmark 10-year Treasury note. The moves have been spurred by the Federal Reserve’s decision to pause its interest rate increases along with investor malaise about the expected pace of economic growth for the rest of the year. That has created an opening for prospective buyers left on the sidelines after rates jumped. Drew Vaughn, of Glastonbury, Conn., locked in a rate of 3.99% this week , after receiving a quote of 4.375% a week ago. That amounts to a saving of more than $1,000 a year in interest. “I was shocked,” he said. The $388,000 mortgage is for a second house he and his wife, Laura, are buying by the beach further south in the state. Mr. Vaughan’s lender, Sanborn Mortgage Corp. in West Hartford, has been advertising the sub-4% rate in recent days, and it has spurred a lot of interest, according to Michael Menatian, the company’s president. “People love it when they have a rate like that,” Mr. Menatian said. “Psychologically, it has a huge impact.” While mortgage rates have fallen, a housing-market rebound faces other obstacles. After a brisk rise in home values in recent years, median prices were unaffordable to the average earner in nearly three-quarters of counties around the country in the first three months of the year, according to an analysis by real-estate data firm Attom Data Solutions. Still, there are signs of newfound interest among prospective borrowers as rates fall. Mortgage applications jumped 8.9% last week from a week earlier, according to the most recent survey by the Mortgage Bankers Association. “It’s such a big move in rates, it’s prompting more potential home buyers to step back into the market,” said Joel Kan, the associate vice president of economic and industry forecasting at MBA. Lower rates also are boosting refinancing applications, which jumped 12% over that span. As of last week, 3.3 million homeowners stood to save money by refinancing their mortgages, the most since January 2018, according to Black Knight Inc., a mortgage-data and technology firm. A renewed boom in the mortgage market would be a benefit to lenders that were hard hit last year as rates rose. Roughly half of mortgages these days are originated by nonbank firms, which, unlike banks, don’t have other lines of business or large balance sheets to fall back on when business dries up. Many depended disproportionately on refinancings and had to slim down or merge as rates rose. The post The 4% Mortgage Is Back appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/real-estate-news/the-4-mortgage-is-back/

Isa Foltin/WireImage “Birdbox” star Sandra Bullock is ready to fly away from her Georgia getaway. The “Ocean’s Eight” actress is listing her oceanfront beach house on Tybee Island for $6.5 million, TMZ has reported. In addition to being an Oscar-winning actress, Bullock also has a keen eye for real estate. The A-lister purchased the vacation home in 2001 for just under $1.5 million. But Bullock has already been reaping financial rewards from her investment. She’s been renting the home out for the last two years, at a whopping $1,400 a night, according to a report in Variety in 2017. Even so, we hope she’s not in a rush to sell. The asking price dwarfs other local homes on the market, with a median listing going for $499,900. With 279 active listings on the market, there are plenty of options to choose from at lower price points.

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com

realtor.com There’s a lot to like here. Especially, if you, like the movie star, need to hide from the madding crowds. A huge selling point is that the compound on almost 3 acres “provides privacy unlike any other on this barrier island,” the listing states. The beachfront estate comes with a total of seven bedrooms and 5.5 bathrooms, with a 3,360-square-foot main home. Luxe perks include a gourmet kitchen, screened porches, a home gym, a basketball court, a pool, and access to a private beach. Plus, the bright and white space has a double-height living room, game area, family room, dining room, and a master suite. The property offers plenty of places to park yourself with a book and look at the beach. The home comes with multiple decks with water views, and a lounge area by the pool. Visitors also receive the star treatment. The 2,848-square-foot guesthouse features its own game room, outdoor grill, and a crow’s nest for taking in the ocean views. And yes, even though the price tag is large, the place does come furnished. With the exception of a few personal items, the listing notes, everything you see in the house is yours. So, along with the special space, you’ll also acquire a bit of Bullock’s decor. And, should you want to leave this beachy paradise, you’re only a 20-minute drive from downtown Historic Savannah. As we’ve previously reported, the 54-year-old owns aserious portfolio of luxury real estate. Along with property inAustin, TX, she also purchased a “legendary” $16.2 million estate in Beverly Hills. She owns two condos in the celeb-filled Sierra Towers in Los Angeles. Plus, there’s reportedly a New York City townhouse, a Victorian in New Orleans, and a cabin in Jackson Hole, WY. Why all the real estate? We’re guessing that as a top-earning actress with a $200 million net worth, Bullock is in the enviable position of having some extra cash to set aside for investments. Maybe she’ll take some time to visit them. As she might say, “Hope Floats.” The post Sandra Bullock Selling Georgia Island Beach House for $6.5M appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/sandra-bullock-selling-georgia-island-beach-house/

Macon, GA: Sean Pavone/iStock We’ve all heard that the housing market is slowing down, giving buyers an edge that many of them believe is long overdue. But that doesn’t mean home prices are actually falling. About 71% of housing markets were still unaffordable for workers earning average wages in the first quarter of 2019, according to a recent report from ATTOM Data Solutions. That’s down a little bit from the previous quarter, at 77%—but it’s still up from 68% a year earlier. (The real estate data firm looked at how much average wage earners would need to make monthly mortgage payments, property taxes, and insurance payments on a median-priced home in 473 counties. The company assumed that they made a 3% down payment on the property with a 28% maximum debt-to-income ratio. Then ATTOM factored in median local wages.) “We are seeing a housing market in flux across the United States,” ATTOM’s Chief Product Officer Todd Teta said in a statement. “[That’s] pricing many people out of the housing market, but also … creating potentially better conditions for buyers.” What are the most affordable housing markets?So where should average Joes and Janes look for homes of their own? Drum roll, please. Bibb County, GA, home to the city of Macon, is a good place to start. This county, about 1.5 hours south of Atlanta, doesn’t boast the lowest prices in the nation, but it’s where folks spent the smallest share of their income on a home. The median home price in the county is just $141,165 as of Feb. 1, according to the most recent realtor.com® data. Handy buyers can scoop up a single-family home in need of some work for around $10,000. That’s doable on a $38,183 median income, according to U.S. Census data from 2013 through 2017. Bibb County was followed by Baltimore, MD, at $265,300; Wayne County, MI, home to Detroit, at $115,050; Rock Island County, IL, at $121,125; and Montgomery County, AL, at $165,000. What are the least affordable housing markets?On the other end of the spectrum are counties where folks are maxing themselves out to become homeowners. Kings County, NY (aka Brooklyn), topped that list. The trendy hipster haven beat out neighboring Manhattan, whose residents tend to make more money and are better able to afford their homes. The median home price in Brooklyn was a steep $849,550. While Brooklyn is known for its drool-worthy brownstones and lofts, it has a wide range of housing, from single-family houses with yards to more modest homes and condos in less affluent areas. Still, Manhattan (aka New York County) wasn’t far behind, earning the second spot on the list. The median price in the borough was nearly double that of Brooklyn, at $1,650,050. It was followed by beachy Santa Cruz County, CA, just south of San Francisco and Silicon Valley, at $899,500; Marin County, CA, just north of San Francisco, at $1,249,550; and Maui County, HI, at $950,050. The post The Most—and Least—Affordable Housing Markets for Average Folks to Buy In appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/best-and-worst-markets-for-average-joes/

Jason Merritt/Getty Images; realtor.com South Florida is well-suited to the lavish lifestyles of the rich and famous. Luxe mansions on waterfront property with palm trees swaying in the distance? That’s what the Sunshine State is all about if you have a few million bucks to spare. Occasionally, South Florida is also a place people love to leave, which is the case for basketball Hall of Famer Scottie Pippen. In fact, he’s been trying to sell his waterfront estate for nearly a decade. The six-time NBA champion initially listed his incredible tropical paradise in 2010 for $16 million, although it was privately offered as far back as January 2009. Since then, it’s been bouncing on and off … and on the market. At one point, the home was offered as a luxury rental for $40,000 a month. Make no mistake: The Venetian-style mansion is gorgeous. It’s located in Harbor Beach, one of Fort Lauderdale’s most exclusive neighborhoods. It comes with views of a sparkling canal that leads straight out to the ocean. The home was conceived and built by award-winning architect Randall Stofft. It has every amenity a baller needs: a sprawling pool, basketball court, gourmet kitchen, game room, media room, and waterfront views.

realtor.com

realtor.com “There are luxury homes with luxury finishes, and then there are true world-class designs,” says William Barrett, a Fort Lauderdale real estate broker. “2571 Del Lago Drive is the latter.” So why hasn’t a buyer stepped up to score Pippen’s luxury abode? Market saturation and movementSouth Florida’s luxury market is healthy, but ever-changing market dynamics seem to be affecting the sale of the home. “Year over year, there’s a pretty staggering difference in inventory,” says Barrett. He told us the luxury market in Fort Lauderdale, including homes priced above $1 million, is always in flux, and added, “Last year there were 299 homes available that meet the luxury requirements for the area. This year there are 378.”

realtor.com Inventory is clearly up, which is nice when buyers are pouring in, but in Fort Lauderdale, “demand has been static for this kind of home.” Which presents a problem when it takes a rarified buyer to begin with. “The luxury market is different,” says South Florida agent Priscilla Haisley. “Especially in our area. It takes a certain kind of buyer who wants a home in Florida that’s at luxury price point, and a lot of those homes don’t move fast.” Barrett agrees. “The sweet spot in this area is a $1 [million] to $3 million price point. Anything more than that can sit for a while before it sells, which isn’t uncommon.” But Pippen’s place has been languishing for years and years. What other factors are at play? Waterfront woes and new construction competitionWhen a buyer thinks of Florida, waterfront property leaps to the imagination. But few buyers are lucky enough to find a waterfront property on the market that meets all of their needs.

realtor.com And unfortunately, Pippen’s property might not check off all the boxes on many luxe wish lists.“The home sits on a couple of lots, but the view is of a canal,” says Barrett. “Don’t get me wrong, it’s a beautiful canal, but a buyer with $10 million to spend is probably going to say they can find a better view for the price.” South Florida is also a prime spot for new construction right now, which can be problematic for the area’s older homes. For a buyer in search of something brand-spanking new, this place isn’t it. “This house was built in 2004 and is relatively unchanged,” says Haisley.

realtor.com Many luxury buyers would rather opt for new construction. “I have a home under contract right now that is similar to this one in lot size, square footage, and features. It’s brand-new and it’s going for about $11 million,” Haisley explains. The trials of top-of-the-line luxuryThough the home is listed for just a hair under $10 million, it hasn’t undergone any major renovations since it was built 15 years ago. “This house was built by one of the top architects in the area, and the finishes and features are all exquisite,” says Barrett. This, he explained, is probably one of the reasons the Pippens haven’t performed any renovations.

realtor.com While appealing, finishes like rare wood accents, high-end flooring, and a waterslide aren’t necessarily every wealthy buyer’s cup of oolong tea. “The finishes in this home are worth every penny, but unfortunately, it’s hard to make a return on them,” says Barrett.

realtor.com So who is going to come along and buy this Italian-inspired beauty? “You’re talking about a white elephant,” said Barrett. “This house isn’t just for the person that can afford it. It’s for the person that can afford to keep it up as well. It’s for someone that understands and appreciates the architecture and the finishes.”

realtor.com The post Why Won’t Anyone Buy Scottie Pippen’s South Florida Mansion? appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/why-wont-anyone-buy-scottie-pippen-south-florida-mansion/

realtor.com A buyer can literally strike gold in Montana for $5.95 million. A modern riverfront home near Big Sky, MT, was constructed with elements brought in from a nearby gold mine. There isn’t any gold dust wafting around, but there are priceless beams on the ceiling and the old tin roof reclaimed from the mine. Oh, and some of the floors are from an old dance hall in Deer Lodge, MT. “I kind of like having a story behind everything,” says the owner/listing agent Scott Altman, who also built the house. Altman bought the 23.33-acre property along the Gallatin River in 2007, and started building the home, near the world-famous Big Sky ski resort. And when his builder heard that they were taking the nearby defunct Gold Coin Mine apart, Altman bought most of what was disassembled. In addition to using the beams and metal roofing, they cut off the face of one of the rock crushers and used it as a fireplace, and used old bolts and chains for the mantel.

realtor.com

realtor.com Then they took the crankshafts from those crushers, erected them vertically, capped them with another old beam, and formed a clever entry gate to the property.

realtor.com They also repurposed the old rails the ore carts used for handrails on the stairs that lead down to the wine cellar.

realtor.com Oh, and then they welded a valve and pipe over a Kohler top-fall faucet that fills the tub in the master bath, so it looks as if the water is falling down from an old mine pipe in the ceiling.

realtor.com The plan was for the Altman family to head for this gold-flecked retreat as soon as their youngest son graduated high school. That’s what they did, finishing and moving into the four-bedroom, 4.5-bath house in 2009.

realtor.com They also outfitted the 5,398-square-foot house with special features, like a pizza oven in the chef’s kitchen (Altman’s family is Italian), a 480-square-foot deck overlooking the water, a family room with an old-timey miners’ bar, and the aforementioned wine cellar, accessed via trap door.

realtor.com Then there’s the gigantic mudroom/gear room/laundry room, crucial in this location. “With all the rafting, hiking, biking, rock climbing, fishing, etc., that you do around here, you realize you need a lot of space for gear,” says Altman.

realtor.com

realtor.com Now, about a decade later, the house isn’t as filled with visitors as it used to be. The Altmans have taken to traveling the country in their Airstream, and Scott says that when they come home, their mine house on the river just feels “too darn big.” So it’s time to downsize, although the Altmans have every intention of staying in the Big Sky area. “We’ve gotten a lot of interest from people who want to use it as a generational compound,” says Altman. It’s easy to see how the property could be ideal for a century or two—or for a celebrity in search of a little pristine privacy. The post This Gorgeous Montana Home Is Made From Pieces of a Gold Mine! appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/unique-homes/gorgeous-montana-home-gold-mine/

Earl Gibson III/Getty Images World Wrestling Entertainment power couple Mike ‘The Miz’ Mizanin and wife, Maryse Ouellet Mizanin, are nimble in the ring and at home. A mere 15 months after closing on their spacious Euro-inspired farmhouse in Austin, TX, they’ve put it back on the market for $2.75 million, which isn’t much more than the $2.6 million listing price it had when they bought it in December 2017. Shortly thereafter, in March, Maryse gave birth to their first daughter, Monroe Sky Mizanin. Last month, the couple announced on live television that they’re pregnant with baby No. 2. But more space for the new addition can’t be the reason they’re selling this 7,770-square foot home. After all, it has five bedrooms, five full baths, and five half-baths. In other words, plenty of room for a family of four.

realtor.com

realtor.com The home is gleaming, with white stucco walls, and arched windows give it the appearance of a grand Mediterranean estate or a modern cathedral.

realtor.com The cathedral theme has been carried into the interior, where two-story ceilings soar above stone walls, arched windows, and passageways, and stone, tile, and hardwood flooring.

realtor.com The rustic design carries into the open, double-island kitchen, with chic antiqued wood cabinetry and beamed ceilings, plus professional-grade appliances. It also features an extensive butler’s pantry.

realtor.com

realtor.com It appears that the couple have made their home a playland paradise for little Monroe. She has not only a pink princess bedroom, but a brightly colored playroom with both a jungle and an aquatic mural.

realtor.com

realtor.com And for the nanny, in-laws, or guests, there’s a self-contained suite with outdoor access and a cozy kitchenette.

realtor.com For entertaining, there’s a game room with a full wet bar. And outdoors, everyone can congregate around the heated, negative-edge pool and spa, or try their luck on the bocce ball court.

realtor.com

realtor.com Mike and Maryse met in 2006 on the “WWE Diva Search” talent competition: He was the host and she was a contestant. Their careers with the WWE have been gaining momentum ever since. Maryse currently serves as The Miz’s manager. They also star in their own reality series, “Miz & Mrs.,” which airs on USA Network. The post Money in the Bank? WWE Superstar The Miz Puts Austin Mansion on the Market appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/wwe-the-miz-austin-mansion/

Sinenkiy/iStock Many thrifty homeowners would rather save a few bucks by taking on upgrades themselves (after a few hours binge-watching HGTV and YouTube tutorials, of course) than by calling in the professionals to install new floors or retile the bathroom. Paying the pros is basically throwing money away, right? If done right, going DIY to fix up a property can lead to some hefty savings. But DIY fails can cost folks big time, according to a recent report from Porch, an online network that connects folks with home improvement professionals.To come up with its results, Porch surveyed nearly 1,200 folks who had completed a home improvement project within the last year. It turns out the average DIY mistake can cost folks $310 to make right. “People often take on repairs themselves in an effort to save money, but often can end [up] spending more,” says Porch’s spokesperson, Amanda Woolley. “People are also underestimating the time and emotional toll of these projects.” So which DIY home improvement flop can set homeowners back the most? Installing flooring wrong costs folks an added $829, bringing the total bill to an average $1,540. That’s got to hurt. Redoing the floors also added an average of 13.8 extra hours of work. “Jobs like flooring have a high material cost, so errors add [up] very quickly,” says Woolley. Hey, hardwood boards don’t come cheap. The second most expensive mistake was in exterior paint jobs, which can add $447 to the tab. This was followed by replacing an electrical outlet wrong, an average $445 blunder; installing a ceiling fan incorrectly, at $306; and messing up the electrical wiring, at $255. Slip-ups can take an emotional toll as well as a financial one. About 45.8% of do-it-yourselfers surveyed who made a mistake fought with their partner during the project, compared with 21.6% of the folks who did everything correctly. Couples were most likely to fight with one another over electrical wiring or rewiring projects, 43.6% of survey respondents reported. Hanging or patching drywall came in second for sparking domestic strife, at 41.7%; followed by replacing an electrical outlet, at 39.1%; installing a ceiling fan, at 38.2%; and an exterior paint job, at 32.7%. “These projects can definitely test relationships—whether they are worried about their partner’s safety or arguing about the materials,” says Woolley. “People need to [be] honest about their skill set and do a very close audit of their time versus money tolerance.” “Is it worth the cost savings for the time and effort you’ll need to put into the job?” she continues. “If not, it might be worth hiring a professional.” The post These Are the Most Expensive Fails in DIY Home Improvement appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/trends/how-much-diy-home-improvement-fails-cost/

iStock Stable housing is increasingly out of reach for many Americans, as both rentals and homes to own grow more expensive and options dwindle. Evictions may be one of the most visible manifestations. Now, a new study shows that not all evictions are created equal. Scholars at Georgia State University, in conjunction with a ProPublica journalist, examined “serial” eviction filings, or those done repeatedly by a landlord against a tenant. By comparing serial evictions to ordinary ones, the researchers found patterns of landlord behavior and intentions, some of which are reminiscent of the worst of the housing crisis a decade ago. As a reminder, nearly half of Americans are “rent-burdened,” which means that they spend more than 30% of their income on rent. Homelessness is on the rise. Nationally, as many as one in seven children may have experienced eviction in the last decade. And, just as the foreclosure crisis disproportionately hit African-Americans, so does the eviction epidemic. Black women in Milwaukee, for example, were evicted at a rate three times their share of the population, and black renters in metro Seattle were evicted four times as frequently as whites there, according to earlier research. The Georgia State authors compiled evidence that eviction proceedings can be predatory: “Filings can be the beginning of a forced removal process, but they are also frequently a tool used to enforce the collection of rent and fees,” they note. The authors cite several earlier local studies that demonstrate the phenomenon. Researchers in Baltimore, Cleveland and Dallas “found that some landlords viewed the additional revenue from late fees, enforced by the threat of an eviction filing, as a supplemental source of funding in addition to the regular rent roll.” Work by Matthew Desmond in Milwaukee suggests that “for every eviction executed through the courts, there are two more that effectively occur outside formal judicial processes. Understanding that eviction is on the table as an outcome, families often vacate their units after marking agreements with landlords.” The Georgia-based authors draw their own conclusions. “Serial filers may cater to tenants who are economically fragile and, like banks charging overdraft fees, they may have identified a way to capitalize on this fragility,” they write. “The effective premium that tenants pay through late fees is a systematic penalty that the lightly regulated rental market inflicts on those who are economically fragile, not dissimilar from the interest rate penalties that subprime lenders inflict on those with previous credit challenges.” One-time evictions are more often used to remove problematic tenants, the authors conclude. But, as noted, the fees collected from serial evictions may either provide additional income for landlords, or provide a means of “disciplining the tenant through state-sanctioned threat of removal.” The use of serial eviction filings as a revenue booster is more likely to be the case among large, professional property managers, rather than mom-and-pop landlords. This is especially important given that property management is trending toward “large corporate ownership,” the authors said. They see a parallel to another trend in the mortgage market, one that had big repercussions in the housing crisis of a decade ago: “The shift from smaller-scale owner-operators to large, corporate owners using larger property management operations is reminiscent of the transition in mortgage lending from primarily portfolio lending (dominated by savings and loans) up through the 1970s to an originate-to-distribute business model in which lenders sold off loans after originating them.” It’s worth noting that many observers of the housing market believe the predatory lending practices that encouraged many people to stretch beyond their means to buy homes, and the failure of policymakers to address the pain experienced by so many Americans as a result, led to populist politics, including the shift driving the 2016 presidential campaign. Indeed, the authors quote an unpublished research paper from Matthew Desmond and others that notes that serial filings can create “psychological strain, social withdrawal and legal cynicism toward the court system.” Based on their examination of evictions in metro Atlanta, which they concede may not represent the nation as a whole or other states in particular, the authors also see patterns in how tenants of different races are treated. While serial filers own property in neighborhoods of diverse populations, those who do not file serially tend to be located in areas with lower African-American populations. What can be done? The authors suggest several policy prescriptions. It’s not enough to make evicting a tenant more expensive, because landlords might simply pass on the higher fees to the tenants. Instead, the authors suggest requiring longer notice periods preceding evictions. Also, requiring or expanding legal representation for tenants could deter serial evictions and also protect tenants. Local governments or housing advocates might also consider making public data on eviction patterns by large landlords. One of the best policy approaches, however, might simply be to “increase the supply of safe and secure affordable housing to low-income tenants,” the authors write. While that goal remains stubbornly challenging, it doesn’t mean local governments, activists, and market participants shouldn’t keep trying. The post The Eviction Crisis Is Starting to Look a Lot Like the Subprime Mortgage Crisis appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/real-estate-news/the-eviction-crisis-is-starting-to-look-a-lot-like-the-subprime-mortgage-crisis/

Stacy Revere/Getty Images Now that NASCAR star Kurt Busch has sped away from the Mooresville, NC, estate known as Chateau de Busch, the driver has listed an additional 138 acres for sale down the road. The huge parcel is available for $7,626,300. While some structures dot the landscape, the property is being sold strictly for its land value. The acreage is “serene wooded and pasture property,” the listing notes. The land affords “boundless opportunity for development in the sought-after Mooresville area.” “This land is strategically placed right within 20 or 30 minutes of everything,” says co-listing agent Kelly Myers. “It’s the perfect canvas for any developer’s vision of new, single-family residential, or even the rarely found estate-sized lots for unique homes.”

realtor.com

realtor.com

realtor.com Busch has deep ties to the area. He purchased a nearby chateau-style retreat in 2013 for $3.29 million. In 2018, he listed the lakefront home for $3.95 million. The Mooresville mansion was eventually sold for $3.6 million. In a 2015 YouTube video for his sponsor, Monster Energy, the professional driver showed off Chateau de Busch. The huge home included a bar, game room, media room, and trophy room. Naturally, a Monster Energy drink was in the fridge. Now that the keys to his kingdom have been passed on, the 40-year-old looks to be shifting gears to an even larger North Carolina deal. But this isn’t the first time the professional racer has tried his hand at selling land. In 2016, the Las Vegas native sought to sell an undeveloped, quarter-acre, oceanfront lot for $1.5 million. That plot is currently off the market. At the same time, Busch was also selling a penthouse at the Residences at the Westin Virginia Beach Town Center. He purchased the three-bedroom, 3.5-bath unit in 2009 for a whopping $2.81 million. He later reduced the price to $1.95 million. Last year he relisted it at $999,999, and it was eventually sold for $920,000. Busch, a 30-time NASCAR race winner, competes full time in the Monster Energy NASCAR Cup Series, where he’s competed in 654 races over 20 years. Along with being the NASCAR Nextel Cup Series champion in 2004, he won the Daytona 500 in 2017. The post NASCAR Star Kurt Busch Is Zooming Away From 138 Acres in North Carolina appeared first on Real Estate News & Insights | realtor.com®. via https://www.realtor.com/news/celebrity-real-estate/nascar-kurt-busch-selling-138-acres-north-carolina/ |

About usI am Casey Abby From USA and I am 30 Year Old. I done my study recently in MBA Marketing. Archives

April 2021

Categories |

RSS Feed

RSS Feed